10 Strategies for Managing Business Risk

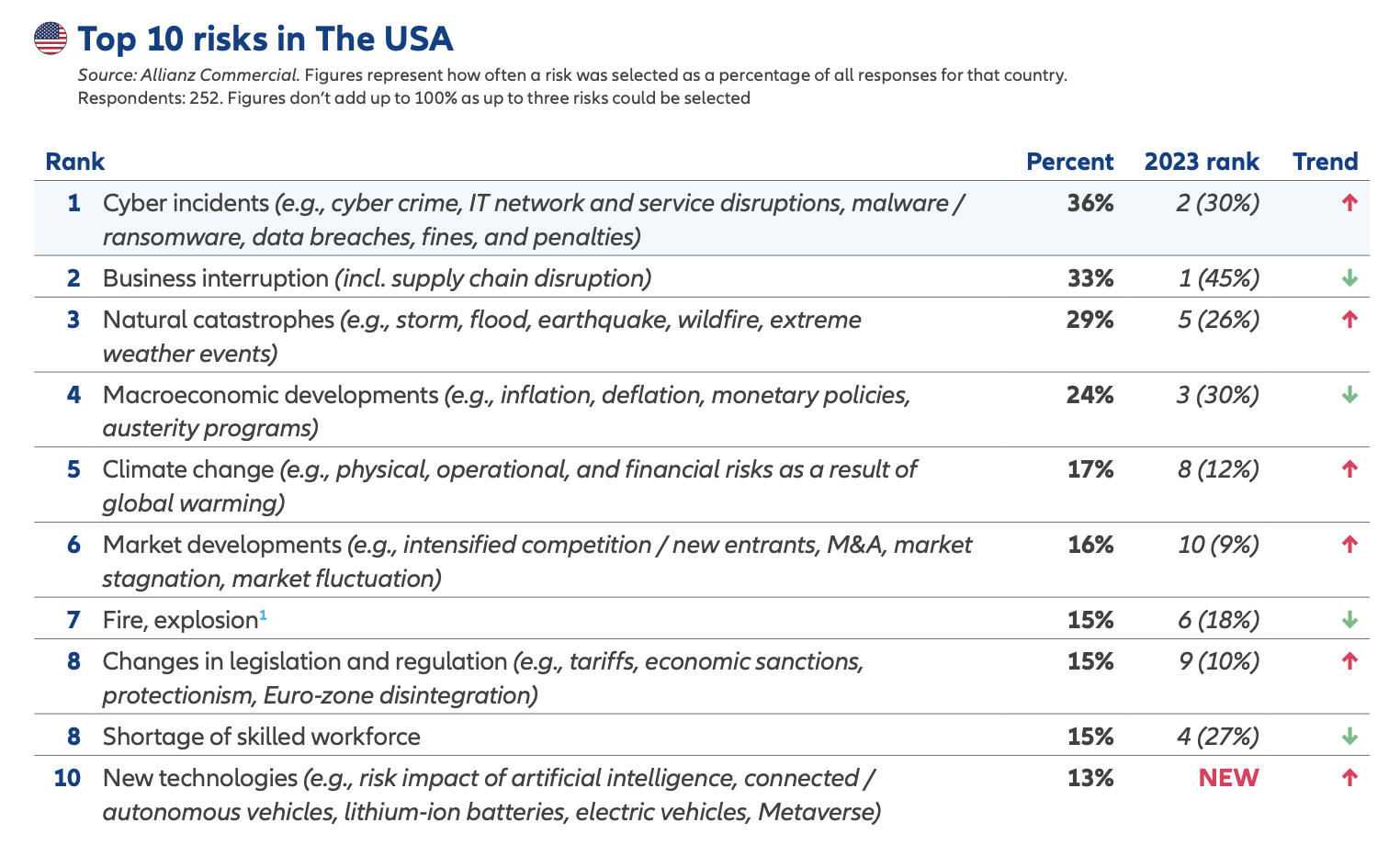

Allianz has released its top ten business risks in the US. Of these risks, Cyber has recently risen to the #1 spot, again signaling the dangers posed by evolving technology. In order to protect your business, consider the current risks, and implement these strategies.

Cyber Incidents: Have a cyber information security officer (CISO) oversee your cyber practices. Preventing cyber breaches is a necessity for any business. In addition, make sure you understand how you are performing relative to your market. Maintain credibility with your customers by meeting their requirements for cybersecurity. If you score well enough, you can continue to build trust with your customers and even enter new markets and gain new revenue.

Business Interruption: Have a business continuity plan that is reviewed and tested quarterly or annually. Create a backup plan for your technology, top products, and top services. If your supply chain gets disrupted, you will want an alternate method to supply these needs. You could also consider having your customers buy key components of critical inventory, and in doing so, share the risk of disruption.

Natural Catastrophe: Keep the disaster recovery portion of your business continuity plan up to date. Have a plan for flexible work locations for your administrative and executive team. In the event that critical facilities of manufacturing or industry are affected, have a plan to quickly assess your operating downtime until normal operations can be restored.

Macroeconomic Developments: Re-evaluate the value you provide to your customers according to the latest monetary developments. Identify the costs of your processes and key tasks, and eliminate the low value systems and processes. Everyone has to lower costs and tune up their value proposition, and this should be a regular exercise for your leadership team.

Climate Change: Cut through the hype and realize that there are always trade-offs to be made. You have to prioritize economic and technological efficiency over sustainability. There are feasible means towards sustainability, for example: buying a more powerful and longer lasting phone or computer, so that you waste less time and material.

Market Developments: Carve out a strength specific to your company, and it will set you apart in the eyes of your customers. Prepare for and meet federal requirements for your line of work, as they are becoming increasingly necessary to do business.

Disaster Recovery: Remember to update your business disaster recovery plan, see above. Hire quality workers who care about your business, people who are conscientious. They will help prevent disaster and be on the look out for danger. One good way to attract them is to be conscientious yourself.

Legislation Changes: First and foremost, be the kind of person who's working to benefit others, not just yourself and business. Benefit your community, be generous, ready to share, and help your employees and your customers grow. Be prepared to spread the good news in your community. Also, talk to your legislators about potential legislative impact to your business, and share what you're doing in your community. If they see your impact, it will incentivize your legislators to work in your favor and encourage more businesses towards good.

Staffing shortages: Hire with a compelling purpose that benefits your staff. Doing great work is better than having great amenities at your workplace. Equip them with good technology and streamlined processes that give them the freedom to do their jobs and bring value to your company.

New technology: Designate a team to focus on the benefits new technology could bring to your company, including AI. Evaluate how evolving technology could effect critical tasks, predictive analysis, and your business model, whether positively or not. Some of these game-changing technologies could reduce major costs, or multiply the value you can create for your customers. Make sure you have someone who can properly analyze and prepare your business.